Disappointing economic data from China, the top oil importer, and the survey showing weaker manufacturing activity across Asia, Europe and the United States raised the risk of an underpowered global economic recovery that would weigh on oil consumption.

China’s declining diesel consumption, as the use of LNG-powered trucks grows, is pressuring domestic fuel demand, while additional risk due to the protracted crisis in the real estate sector remains.

The world’s second-largest economy has long been the growth engine for global oil demand, but its increasing need for transport fuels as the energy transition gathers pace is now dampening world markets.

According to the IEA’s July oil market report, global oil demand growth in the second quarter was the slowest since the end of 2022 due to lower consumption in China.

Weak demand from manufacturing and construction is expected to persist in the second half of the year as the world’s largest oil importer grapples with a sluggish real estate sector, which accounts for about 70% of household wealth.

As increasing numbers of LNG trucks undermine demand for diesel, accelerating sales of electric vehicles indicate that China’s demand for transport fuel is nearing its peak. Gasoline and diesel make up more than 40% of the country’s oil demand.

The International Energy Agency has been revising down its 2024 oil product demand forecast for China on a monthly basis.

At the same time, tensions are once again rising in the Middle East. This could lead to a military conflict and jeopardize oil supply routes.

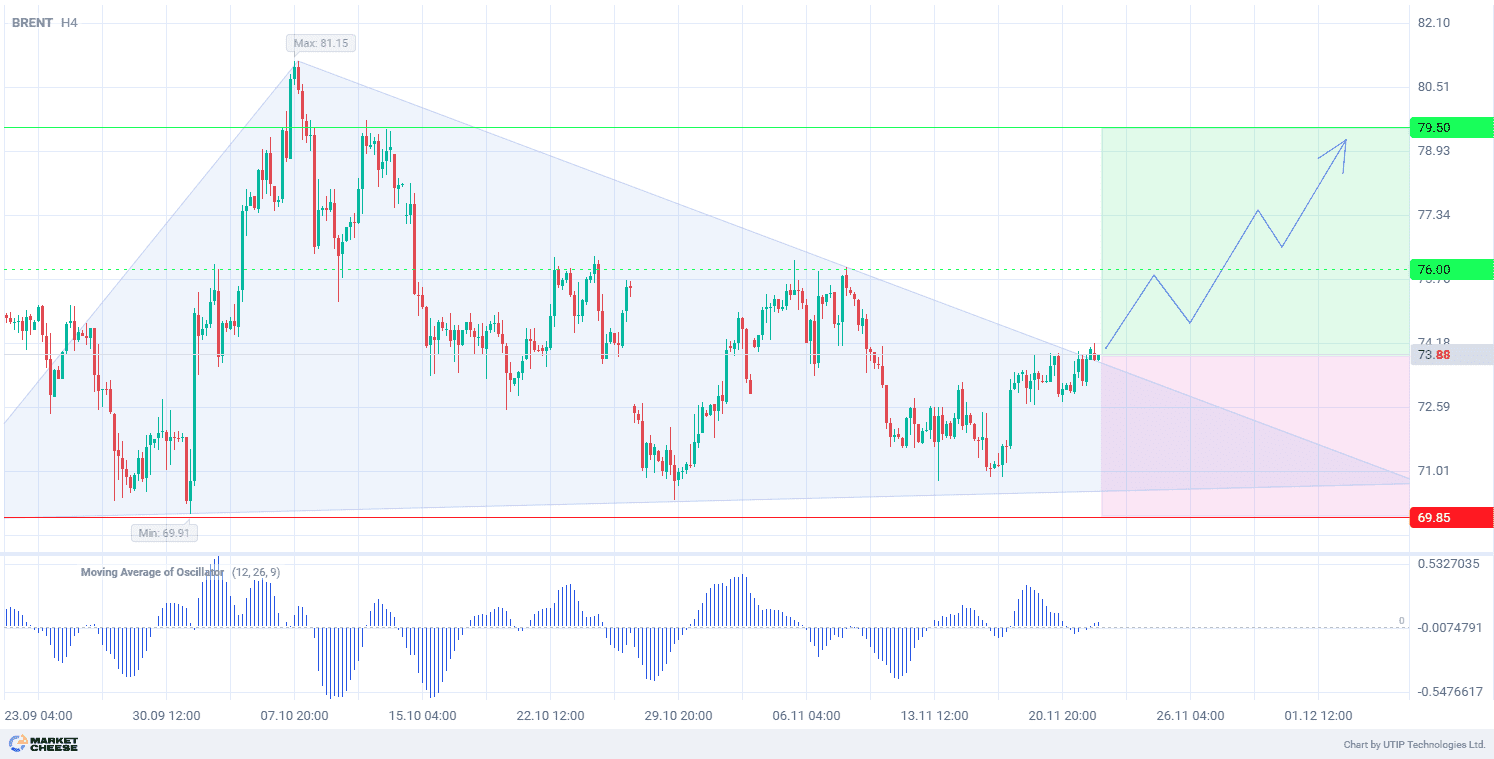

From a technical point of view, Brent oil is now at the resistance level of 79.5 dollars per barrel. Therefore, the most probable short-term scenario is a pullback of Brent prices up to the level of 81.1.

The final recommendation is to buy Brent from the level of 79.5.

Profits should be taken at the level of 81.1. A Stop loss could be set at the level of 78.8.

The possible loss should not exceed 2% of your deposit funds.